Wealth-Ready Blueprint

Stop guessing with your money. Start building real wealth.

Two no-fluff courses — Debt Management + Personal Finance 101 — that hand you the exact system to kill debt, control cash flow, and grow what you keep. Lifetime access. One payment. Zero excuses.

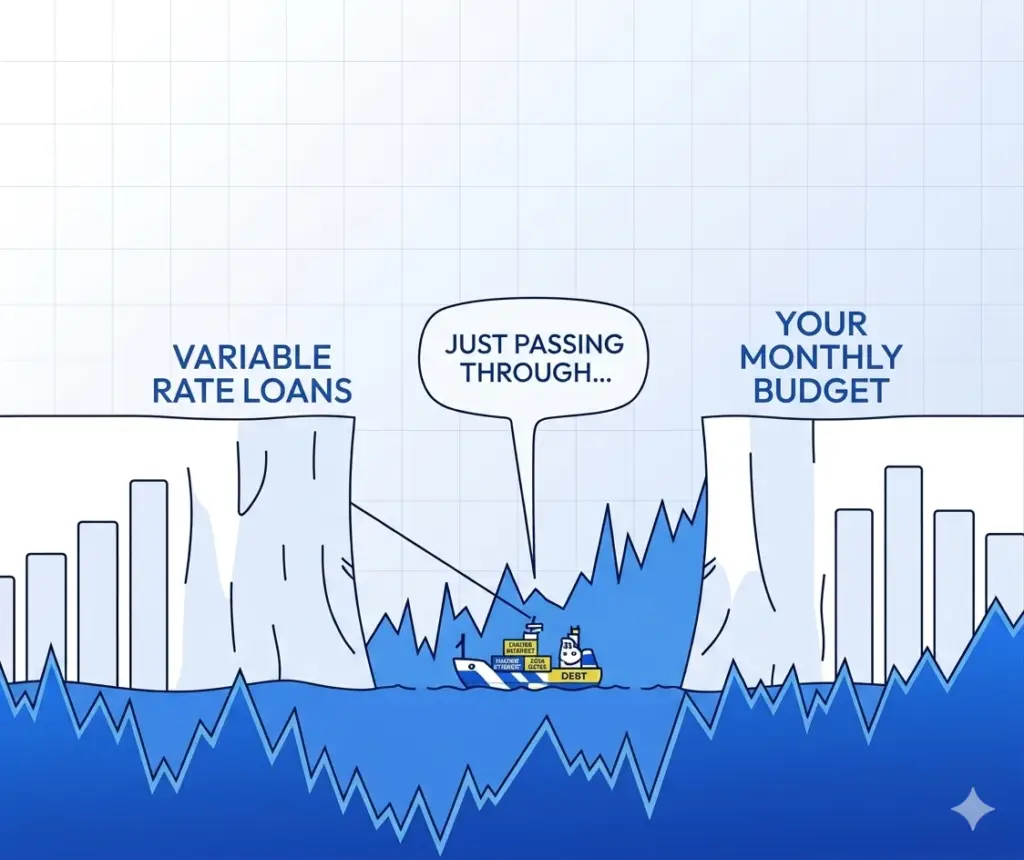

Debt Management

Personal Finance 101

€9.99

— less than a coffee & a croissant. One payment. Yours for life.

Get Instant Access →